Choosing the right life insurance policy can feel like standing at a financial crossroads. You are balancing the immediate need to protect your family with long-term financial goals. The two most common paths you will encounter are universal life insurance and term life insurance.

To make an informed decision, you need an objective breakdown of how these policies function. This comprehensive audit will dissect the mechanics of both options, comparing their costs, flexibility, and unique features.

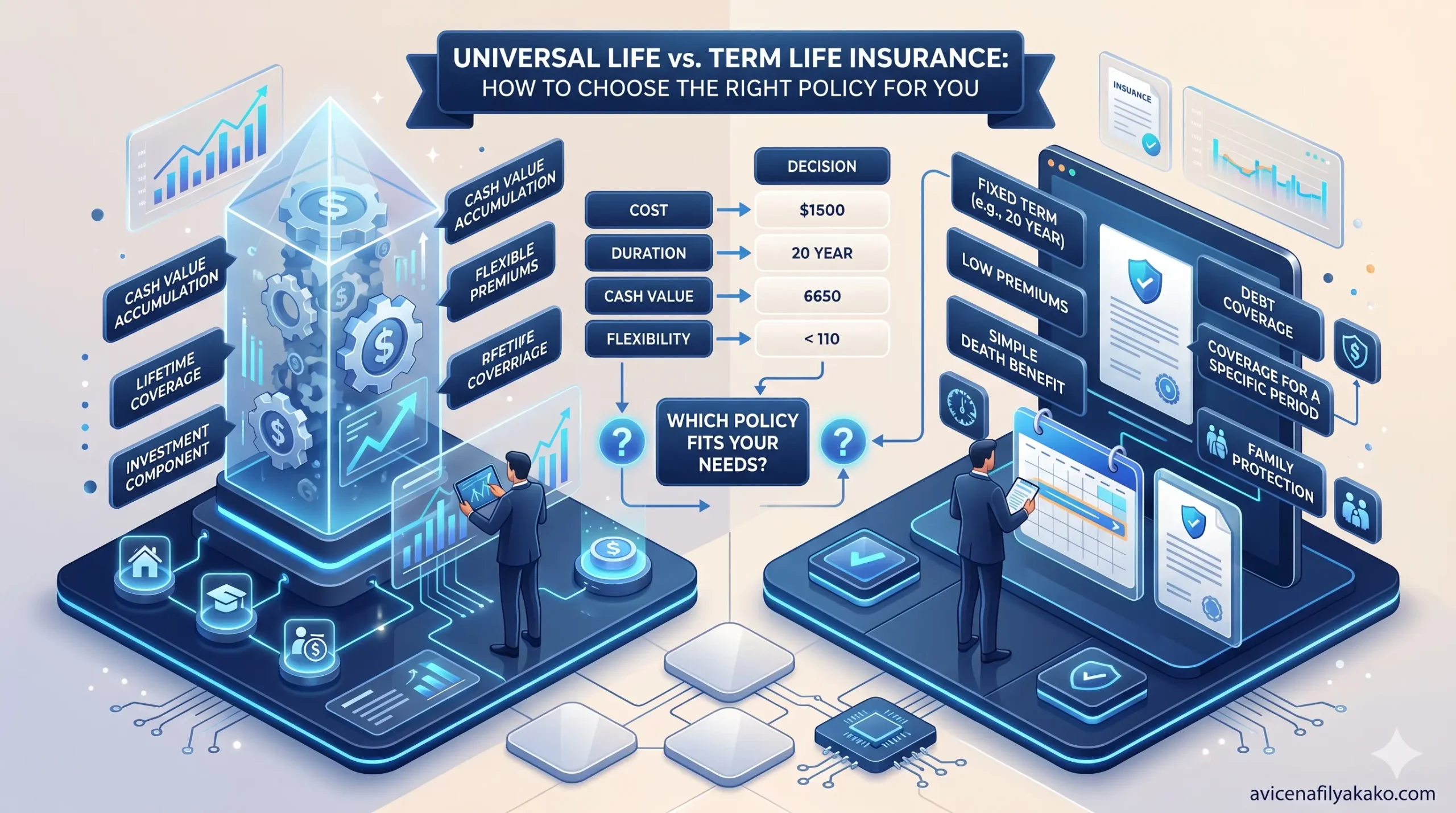

Understanding the Core Mechanics of Life Insurance

Before diving into the specific policy types, it is essential to understand the foundational elements of life insurance. At its core, any policy is a contract between you and an insurance provider. In exchange for regular payments, the insurer promises a financial safety net for your beneficiaries.

As noted by financial experts at New York Life, choosing between permanent and temporary coverage depends heavily on your current stage of life and long-term wealth strategy. You can explore their detailed breakdown of these foundational concepts through the New York Life Insurance Guide.

What is Term Life Insurance?

Think of term life insurance like renting a house. You pay for the right to occupy the space for a specific period, but you do not build equity. If you move out (or if the policy expires), you walk away with nothing.

The Pillars of Term Coverage

- Fixed Life Insurance Duration: You select a specific life insurance term, typically spanning 10, 20, or 30 years.

- Pure Protection: The policy exists solely to pay out a death benefit if you pass away within the active window.

- Predictable Premium Costs: Your monthly or annual payments remain locked in and guaranteed for the entire life insurance term.

Because it lacks complex investment features, term coverage offers the most straightforward form of financial protection available on the market today.

What is Universal Life Insurance?

If term insurance is like renting, universal life insurance is akin to buying a home with a flexible mortgage. It is a form of permanent coverage designed to last your entire lifetime, provided the required payments are met.

The Mechanics of Universal Coverage

- Cash Value Accumulation: A portion of your premium goes into a built-in cash value account, which grows tax-deferred over time.

- Flexible Premium Costs: Unlike rigid permanent policies, universal coverage allows you to adjust your payments up or down based on your current financial situation.

- Adjustable Death Benefit: You can often increase or decrease the payout amount as your familial needs evolve.

As legendary investor Warren Buffett famously noted:

“Risk comes from not knowing what you’re doing.”

Universal coverage reduces long-term risk by offering a permanent safety net that adapts to your changing financial climate. Because the built-in cash value accumulates over time, integrating this permanent policy into your broader financial blueprint requires aligning it with proven strategic asset allocation models to optimize long-term wealth growth.

Side-by-Side Comparison: Term vs. Universal

When deciding which path to take, comparing the core metrics side-by-side helps clarify which structure aligns with your financial plan.

| Feature | Term Life Insurance | Universal Life Insurance |

| Coverage Lifespan | Temporary (10–30 years) | Permanent (Whole life) |

| Cash Value Component | None | Yes (Tax-deferred growth) |

| Premium Flexibility | Strictly Fixed | Adjustable |

Data analyzed by international wealth managers underscores that the right choice hinges on whether you view coverage as a temporary safety net or a lifelong asset. For an international perspective on these structural differences, review the Sun Life Comparison Audit.

Strategic Playbook: Which Choice Fits Your Goals?

Selecting a policy is not about finding the “best” product overall, but finding the best tool for your specific financial blueprint.

When to Choose Term Coverage

You should lean toward a term policy if you want maximizing protection at the lowest possible cost. It is ideal for young families who need to cover specific, temporary liabilities. For instance, you might choose a 20-year life insurance term to match the lifespan of a home mortgage or to protect your children until they graduate from college.

When to Choose Universal Coverage

Universal coverage serves you better if you view life insurance as a component of a broader estate planning strategy. High-net-worth individuals often utilize the growing cash value to build an asset that can be borrowed against during their lifetime. It also ensures a guaranteed death benefit to cover estate taxes or inheritances, no matter how long you live. To maximize the protection of these assets, many policyholders choose to pair permanent coverage with other estate planning tools, allowing them to explore revocable living trust benefits for seamless wealth transfer to their beneficiaries.

Frequently Asked Questions

Can I convert a term life insurance policy into a universal life policy?

Yes, many insurance providers include a term conversion rider that allows you to transition your temporary policy into permanent coverage without undergoing a medical exam.

What happens to the cash value in a universal life policy when I die?

Generally, the accumulated cash value reverts to the insurance company upon your death, and your beneficiaries receive only the face value of the death benefit, unless you purchased a specific rider that pays out both.

Does term life insurance have any cash value?

No, term insurance is pure protection and does not accumulate any cash value or investment equity during the life insurance duration.

Disclaimer: The information provided in this article is for educational and general informational purposes only and should not be construed as professional advice (such as legal, medical, or financial). While the author strives to provide accurate and up-to-date information, no representations or warranties are made regarding its completeness or reliability. Any action you take based on this information is strictly at your own risk.

This article was authored by Avicena Fily A Kako, a Digital Entrepreneur & SEO Specialist using AI to scale business and finance projects.