High earners frequently hit a brick wall when attempting to build tax-free wealth. The IRS strictly limits who can contribute directly to a Roth IRA based on income. If your income exceeds those thresholds, you might feel locked out of one of the best retirement vehicles available.

Fortunately, a legal loophole known as the Backdoor Roth IRA allows high income earners to bypass these restrictions. Think of it like a VIP venue with a closed front door, but the bouncer points you toward an open side entrance.

By executing a specific multi-step strategy, you can legally fund a Roth account regardless of how much money you make. This comprehensive log breaks down exactly how to navigate the process safely and efficiently.

What is a Backdoor Roth IRA?

A Backdoor Roth IRA is not a specific type of investment account. Instead, it is a financial strategy used by high earners to convert traditional IRA contributions into Roth IRA contributions.

Normally, if your modified adjusted gross income (MAGI) crosses the IRS threshold, your ability to contribute directly to a Roth IRA phases out completely. However, there are no income limits on making non-deductible contributions to a traditional IRA, nor are there income limits on converting those funds to a Roth.

“The backdoor Roth IRA strategy remains one of the most effective tax-planning tools for high-earning professionals looking to maximize their tax-free growth potential,” notes financial expert Ed Slott, CPA.

By utilizing this method, you ensure your money grows tax-free and can be withdrawn tax-free during retirement.

Step-by-Step Guide to Executing the Strategy

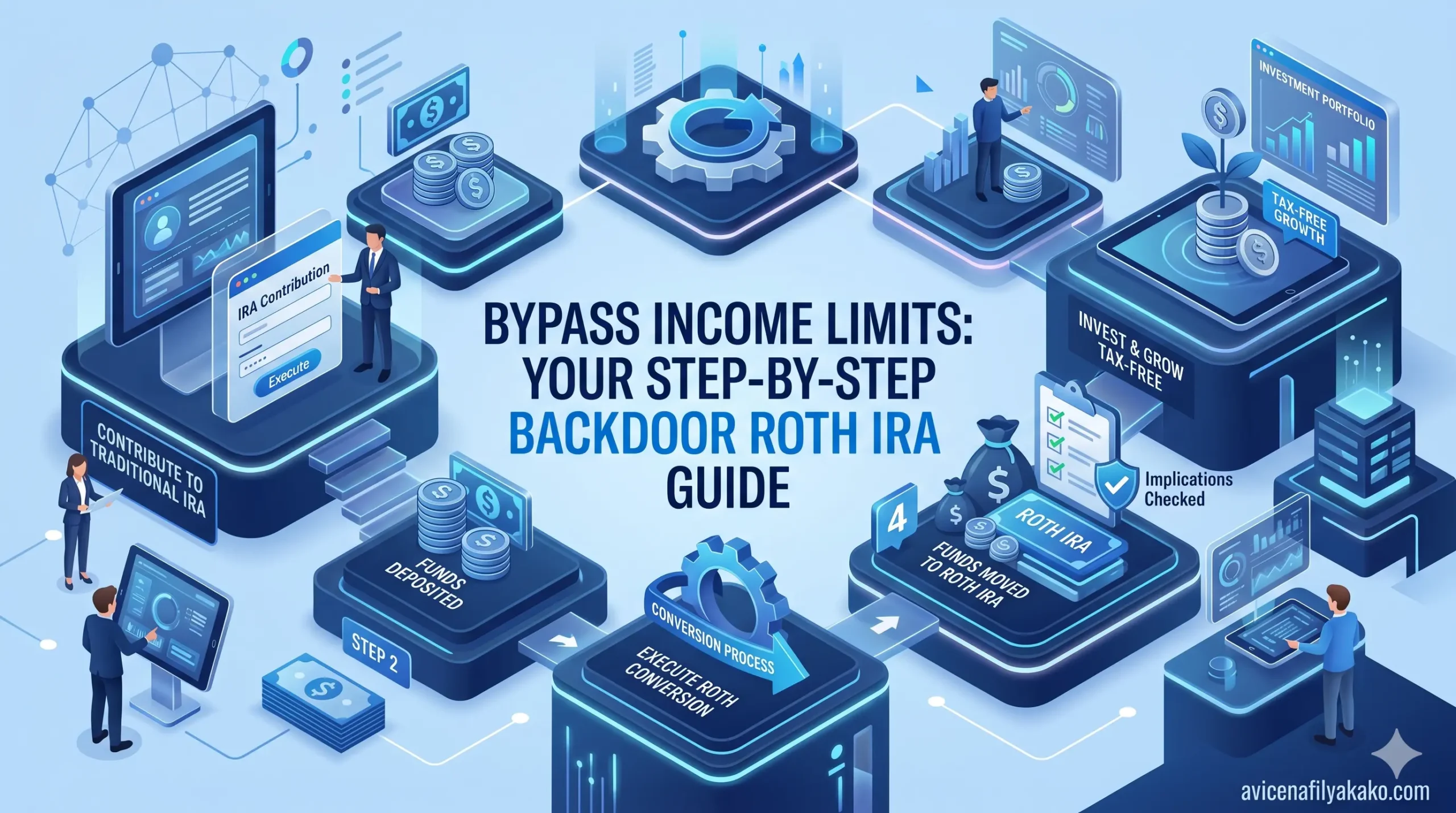

Executing a Backdoor Roth IRA requires precision. Moving money incorrectly or miscalculating your tax liability can result in unwanted IRS penalties. Follow these four clear steps to complete the process.

Step 1: Open and Fund a Traditional IRA

First, you need to open a traditional IRA with a brokerage firm if you do not already have one. You will then make a non-deductible contribution up to the maximum annual limit allowed by the IRS. For more detailed instructions on initiating this account setup, you can review Vanguard’s Step-by-Step IRA Guide.

Step 2: Leave the Funds in Cash

Once the money lands in your traditional IRA, do not invest it in stocks or mutual funds. Keep the contribution sitting as cash or in a money market fund. You want to avoid any market gains during the short window before the tax conversion, as any earnings generated will be subject to income tax when you move the money.

Step 3: Request a Roth IRA Conversion

After the funds clear—usually within a few business days—instruct your brokerage firm to perform a tax conversion of your entire traditional IRA balance into a Roth IRA. Most modern brokerages allow you to initiate this transfer online with a single click. This action officially moves your funds into the tax-free wrapper of the roth ira.

Step 4: File Form 8606 with Your Taxes

The final, crucial step happens during tax season. You must report your non-deductible contribution and subsequent conversion to the IRS using Form 8606. This form tracks your basis in the traditional IRA and proves to the IRS that you already paid taxes on the initial contribution, ensuring you are not taxed twice.

Navigating the Pro-Rata Rule Pitfall

The biggest trap in the back door roth ira process is the IRS pro-rata rule. The IRS does not view your individual traditional IRA accounts in isolation. Instead, it aggregates all your traditional IRAs, SEP IRAs, and SIMPLE IRAs to determine your tax liability.

If you possess a mix of pre-tax (deductible) and post-tax (non-deductible) funds across any traditional IRA accounts, you cannot choose to convert only the post-tax money. The IRS requires your conversion to be proportional to your total balance.

| Total Pre-Tax IRA Funds | Total Post-Tax IRA Funds | Percentage of Conversion Subject to Tax |

| $0 | $7,000 | 0% (Fully Tax-Free) |

| $21,000 | $7,000 | 75% (Only 25% is Tax-Free) |

If you have significant pre-tax money in an existing IRA, you may want to consider a “reverse rollover.” This process rolls your pre-tax IRA funds into an active employer 401(k) plan, clearing the path for a clean, tax-free Backdoor Roth IRA. Beyond this specific strategy, it is equally important to understand how tax-efficient asset location minimizes your overall portfolio drag across all investment accounts.

Comparing Your IRA Options

Understanding the mechanics of a Backdoor Roth IRA requires a clear picture of how it differs from standard retirement accounts. Data from Investopedia’s Deep Dive on Backdoor Roth IRAs highlights how these account structures handle income restrictions and future withdrawals differently.

- Traditional IRA: Contributions may be tax-deductible, but withdrawals in retirement are taxed as ordinary income.

- Direct Roth IRA: Contributions are made with after-tax dollars, and withdrawals are 100% tax-free, but high earners are barred from contributing.

- Backdoor Roth IRA: Bypasses direct income caps by converting after-tax traditional contributions into a Roth structure, granting high earners identical tax-free retirement benefits.

Frequently Asked Questions

Is the Backdoor Roth IRA legal?

Yes, the Backdoor Roth IRA is completely legal and was officially recognized by Congress under the Tax Cuts and Jobs Act of 2017. Financial institutions routinely facilitate these conversions, provided savers accurately document the transactions on their annual tax returns.

How long do I have to wait before converting the funds?

You do not have to wait a specific length of time, and most financial advisors recommend initiating the conversion as soon as your traditional IRA contribution clears. Converting the funds quickly minimizes the chances of the money earning interest, which simplifies your tax reporting.

Can I execute a Backdoor Roth IRA if I have a 401(k)?

Yes, you can execute a Backdoor Roth IRA even if you actively participate in an employer-sponsored 401(k) plan. Workplace 401(k) accounts do not count toward the aggregate balances used in the IRS pro-rata calculation, making this an ideal stacking strategy for high earners. To further optimize your tax-sheltered wealth, you can also combine this with an HSA triple tax advantage strategy to maximize your health and retirement savings simultaneously.

Disclaimer: The information provided in this article is for educational and general informational purposes only and should not be construed as professional advice (such as legal, medical, or financial). While the author strives to provide accurate and up-to-date information, no representations or warranties are made regarding its completeness or reliability. Any action you take based on this information is strictly at your own risk.

This article was authored by Avicena Fily A Kako, a Digital Entrepreneur & SEO Specialist using AI to scale business and finance projects.