The U.S. Department of Education is executing a comprehensive structural overhaul of the federal student loan system that will permanently eliminate the Saving on a Valuable Education (SAVE) plan and reduce repayment options for future borrowers starting July 1, 2026. Triggered by a federal court-approved settlement following a March court order that halted the program, the transition forces roughly 7.5 million active borrowers to manually select a alternative legal repayment framework within a strict 90-day window. Failure to act within this timeline will result in automatic enrollment into either the traditional Standard Repayment Plan or a new Tiered Standard plan.

The stakes of this regulatory pivot extend far beyond simple paperwork updates. For millions of individuals, missing the pre-July 1 cutoffs means risking higher monthly bills, a permanent loss of income-driven protections, and a complete freeze on certain public service forgiveness tracks. Furthermore, the policy tightens front-end borrowing limits for graduate students and families, fundamentally shifting the mechanics of higher education financing.

Digital tracking indicates that Federal Student Aid has already initialized its mass email and phone outreach campaigns as of June 8, 2026. This immediate wave of notifications has generated noticeable spikes in user traffic on the studentaid.gov server networks, signaling that the scramble for compliance has begun.

News Analysis: A Strategic Shift in Federal Capital Flow

From an analytical standpoint, this sudden overhaul represents a sharp retrenchment by the federal government away from expansive, highly subsidized student loan repayment structures. By terminating the SAVE plan and introducing the more constrained Repayment Assistance Plan (RAP), policymakers are shifting a heavier, long-term financial burden back onto high-balance borrowers, particularly graduate students and parents.

The introduction of rigid annual and lifetime caps appears to be an attempt by the Department of Education to artificially constrict the flow of easy federal capital into higher education institutions, potentially as a mechanism to curb systemic tuition inflation. However, I expect the immediate consequence for everyday borrowers will be a severe administrative bottleneck. Because millions of accounts are moving simultaneously, individuals who delay their applications face a high probability of severe processing delays and unexpected cash-flow shocks.

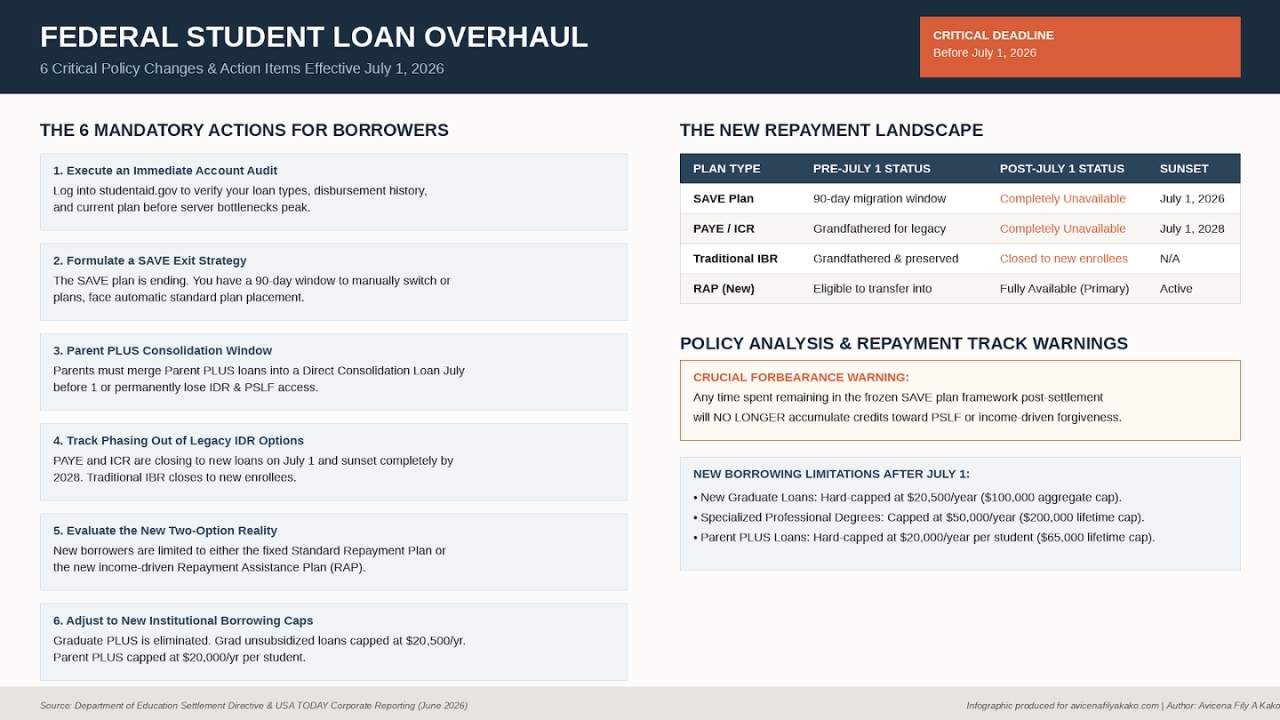

The Six Mandatory Actions for Borrowers

To protect your financial trajectory before the new student loan rules take hold, borrowers must navigate six distinct regulatory changes.

1. Execute an Immediate Account Audit

Borrowers should log in to the official studentaid.gov portal immediately to confirm their current loan types, exact repayment plan enrollment, and disbursement histories. Jack Wallace, the director of government and lender relations at Yrefy, noted that borrowers may currently qualify for specific programs that will completely close after the deadline, meaning that waiting will narrow available choices.

2. Formulate a SAVE Exit Strategy

If you are enrolled in the SAVE plan, do not assume your status is secure. Servicers are beginning a 90-day countdown to transition borrowers out of the defunct program. Stacey MacPhetres, an expert with Bright Horizons, strongly encourages borrowers to apply for alternative income-driven plans before the automatic deadline because standard options often demand much higher monthly cash outlays.

Crucially for those tracking Public Service Loan Forgiveness (PSLF) or income-driven milestones, MacPhetres clarified that any ongoing payments made while remaining in the frozen SAVE framework will no longer count toward forgiveness progress. Eligible borrowers must actively look to switch to plans like the traditional Income-Based Repayment (IBR) system.

3. Meet the Hard Parent PLUS Consolidation Deadline

For parents holding Parent PLUS loans, the upcoming structural cliff is absolute. Borrowers must successfully merge these accounts into a Direct Consolidation Loan prior to July 1 to maintain access to income-driven repayment structures and the PSLF track. Missing this date results in a permanent loss of IDR eligibility, locking families into traditional standard repayment terms.

4. Track the Phasing Out of Legacy IDR Options

The menu of available income-driven choices is shrinking significantly. Both the Pay As You Earn (PAYE) and Income-Contingent Repayment (ICR) frameworks will be completely unavailable for any new loans disbursed on or after July 1. Furthermore, both programs are scheduled to sunset entirely by July 1, 2028, requiring current participants to shift to a new plan by June 30, 2028. Traditional IBR will remain grandfathered for older, pre-July disbursements but will lock its doors to new enrollees on July 1.

| Repayment Plan | Status for Existing Loans (Pre-July 1) | Status for New Borrowers (Post-July 1) | Ultimate Program Sunset |

|---|---|---|---|

| SAVE Plan | 90-day mandatory migration window | Completely Unavailable | July 1, 2026 |

| PAYE / ICR | Grandfathered for legacy disbursements | Completely Unavailable | July 1, 2028 (Full phase-out) |

| Traditional IBR | Grandfathered and preserved | Closed to new enrollees | N/A (Closed system) |

| RAP (New) | Eligible to transfer into | Fully Available | Active |

5. Evaluate the New Two-Option Reality for Future Borrowers

Starting July 1, individuals entering the federal student aid system for the first time will face a highly simplified, binary choice for repayment:

- The Standard Repayment Plan: Features fixed monthly payments across a 10-to-30-year window. While this plan results in higher immediate monthly bills, it minimizes the total interest accumulated over the lifespan of the debt.

- The Repayment Assistance Plan (RAP): Serving as the new primary income-driven option, RAP ties monthly bills to a range of 1% to 10% of a borrower’s adjusted gross income (AGI). The Department of Education specifies that RAP scales down to a minimum payment of $10 per month for individuals earning under $10,000 annually, with ultimate debt forgiveness occurring after 30 years of compliant payments.

6. Adjust to New Institutional Borrowing Caps

The policy overhaul simultaneously caps the total volume of incoming federal debt. Graduate PLUS loans will be permanently terminated for new applicants after July 1. Existing graduate students can maintain access to older limits for up to three academic years only if they received at least one loan disbursement prior to the cutoff date.

New direct unsubsidized graduate borrowing will be strictly capped at $20,500 annually with a $100,000 lifetime ceiling for standard graduate degrees, or $50,000 annually with a $200,000 lifetime maximum for specialized professional tracks. Concurrently, Parent PLUS loans will face a rigid threshold of $20,000 per year per student, alongside a permanent $65,000 lifetime cap per dependent. To borrow under the legacy, higher limits, an application must be approved and achieve a formal financial disbursement before the July 1, 2026 deadline.

What You Need to Know (FAQ)

What happens to my account if I am currently enrolled in the SAVE plan?

Borrowers currently in the SAVE plan will be contacted by their loan servicers and given a strict 90-day window to manually select a new repayment option. If you do not choose a new plan within this timeframe, the Department of Education will automatically transition your account into the Standard Repayment Plan or the new Tiered Standard plan.

Can I remain in the SAVE plan while my loans are in forbearance?

While you may temporarily remain in forbearance as the system transitions, the Department of Education has clarified that any time spent in SAVE post-settlement will no longer count as credit toward Public Service Loan Forgiveness (PSLF) or income-driven forgiveness milestones. To keep making progress, eligible borrowers must actively apply to transition into an alternative framework like IBR.

What happens if a parent misses the July 1 consolidation deadline for Parent PLUS loans?

Missing the July 1 deadline means the borrower permanently loses access to all federal income-driven repayment options and the Public Service Loan Forgiveness program. The outstanding debt will be permanently restricted to traditional standard repayment plans, which typically demand substantially higher monthly out-of-pocket payments.

Next Steps in the Transition

The Department of Education via Federal Student Aid has already initiated direct phone and digital notifications to affected accounts. As processing queues lengthen ahead of the July 1 deadline, the immediate priority for any individual holding federal debt is to submit consolidation paperwork and alternative plan applications through studentaid.gov to avoid automatic enrollment defaults.

Disclaimer: This article is provided for general informational and news purposes only and should not be construed as professional advice (such as legal, medical, or financial). The author strives for accuracy and timeliness, but no representations or warranties are made regarding completeness or reliability, and details may change as a story develops. Any action you take based on this information is strictly at your own risk. Corrections or updates can be requested via the site’s contact page.